They have become the modern investor's watchword, from the largest asset manager to the teenager opening a first account: ETFs. By mid-2026 total ETF assets worldwide hit a record $23.09 trillion, with year-to-date net inflows of $1.33 trillion — the strongest first half ever (ETFGI data). Behind the acronym lies a simple, powerful idea. Let's unpack it, without jargon.

What ETFs are

ETF stands for Exchange Traded Fund. The clearest image is a basket: a single instrument holding tens, hundreds or thousands of securities inside it — stocks, bonds, commodities. By buying one ETF share, you buy a slice of everything in the basket at once.

Most ETFs are passively managed: they don't try to beat the market, they replicate it. An S&P 500 ETF simply aims to track the 500 largest U.S. companies. The manager doesn't pick "winners": it copies the index. Hence the low costs, which are the real heart of their success.

How they work: traded like a stock

The feature that sets them apart from traditional mutual funds is in the name: they are traded on an exchange. That means an ETF share can be bought and sold throughout the day, at a price that moves in real time, just like a stock. A "classic" mutual fund, by contrast, trades only once a day at its closing value.

Behind the scenes, a creation and redemption mechanism run by large intermediaries keeps the ETF's price almost always aligned with the real value of the securities it holds. For the ordinary investor the technical detail matters little; what matters is the result: liquidity and fair prices.

Why they're so popular (especially with beginners)

- Instant diversification: with a few dozen euros you own hundreds of companies. Single-stock risk is diluted.

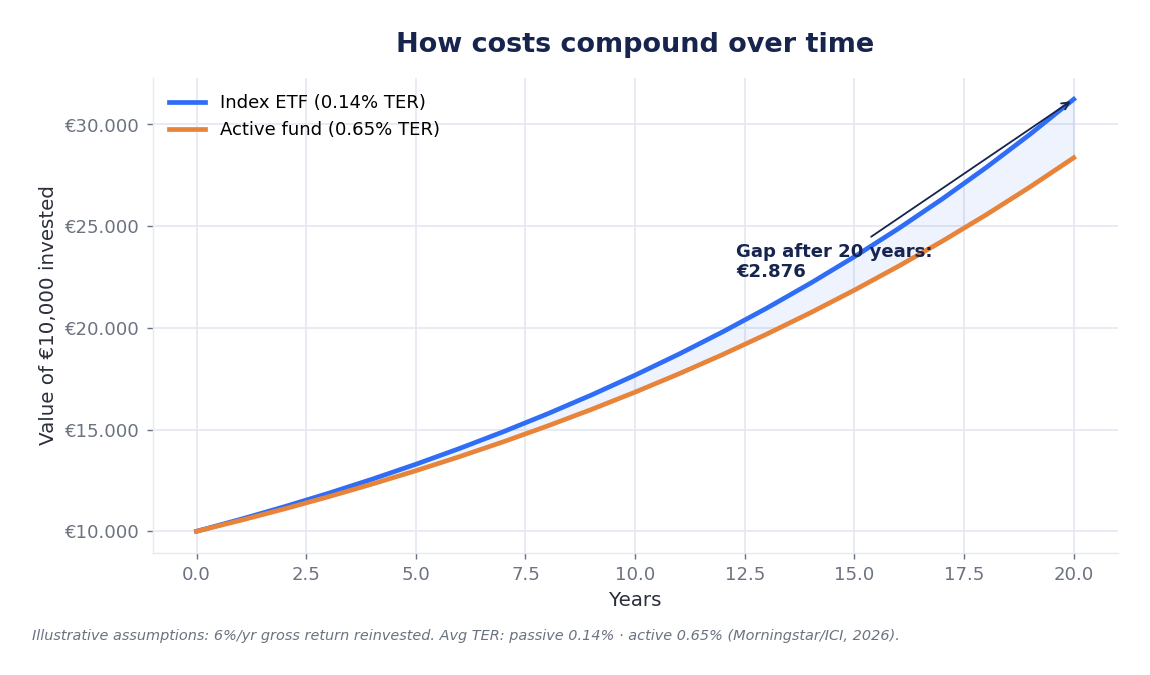

- Low costs: this is where the game is won. The annual cost (TER) of an index ETF averages 0.14%, against 0.65% for an actively managed equity fund. It sounds trivial: it isn't.

- Transparency: you always know what the basket holds and which index it tracks.

- Accessibility: they can be bought from any brokerage account, even in small amounts and through periodic savings plans.

Why costs matter more than you think

Half a percentage point a year sounds negligible. But over long horizons, through compounding, that small erosion becomes a chasm. The chart below shows how €10,000 invested for 20 years at the same gross return would behave, changing only the cost of the instrument.

ETFs versus active funds: what the data say

The natural question: surely a skilled manager beats an index? The data say that, over the long run, almost no one does so consistently. According to S&P Dow Jones' SPIVA Scorecard, in 2025 79% of U.S. large-cap equity funds underperformed the S&P 500; and over 15-year horizons there is not a single category in which most active managers beat their benchmark.

| Feature | Index ETF | Active mutual fund |

|---|---|---|

| Average annual cost (TER) | ~0.14% | ~0.65% |

| Trading | On-exchange, real time | Once a day |

| Goal | Replicate the index | Beat the index |

| Basket transparency | High (daily) | Periodic |

| Beats the index long term? | By design it tracks it | Rarely (SPIVA data) |

What to know before you start

ETFs are not risk-free, and they are not all alike. Some points to watch:

- Market risk remains: an ETF diversifies across securities, but if the whole market falls, so does the ETF. It is not a guaranteed piggy bank.

- Accumulating or distributing: accumulating ETFs reinvest dividends (useful for compounding), distributing ones pay them out to you.

- Currency risk: an ETF on dollar-denominated securities exposes you to euro/dollar swings.

- Beware the exotic "ETFs": leveraged, inverse or ETN/ETC products carry very different risks from a classic diversified equity ETF. For beginners, broad indices are safer.

For many small savers the most sensible approach is a regular savings plan into a broad, diversified ETF: small amounts invested consistently, letting time and compounding do the work.

The bottom line

ETFs have democratised investing: diversification, low costs and transparency in a single instrument. They are not magic — market risk stays — but the mix of simplicity and low cost explains why they have become the building block of so many portfolios, from beginners to large institutions.

Disclaimer: this article is for information and educational purposes only and does not constitute financial advice. Any investment decision should be assessed against your own circumstances and, if needed, with a qualified professional.