"Don't put all your eggs in one basket." It is finance's most quoted proverb, and for good reason: in a few words it captures one of the few principles that truly work. Diversification is often called the only "free lunch" in investing, because it lets you reduce risk without necessarily giving up expected return. But it is not magic: it has precise mechanics and equally precise limits.

What diversification is

To diversify means spreading capital across several investments that differ from one another, so that a poor performance in one can be offset by another. The idea was formalised in the 1950s by economist Harry Markowitz, whose work on "modern portfolio theory" earned him the Nobel Prize in 1990. His insight: what matters is not the risk of a single security, but how securities move together.

Why it works: specific risk and market risk

An investment's risk can be split into two parts:

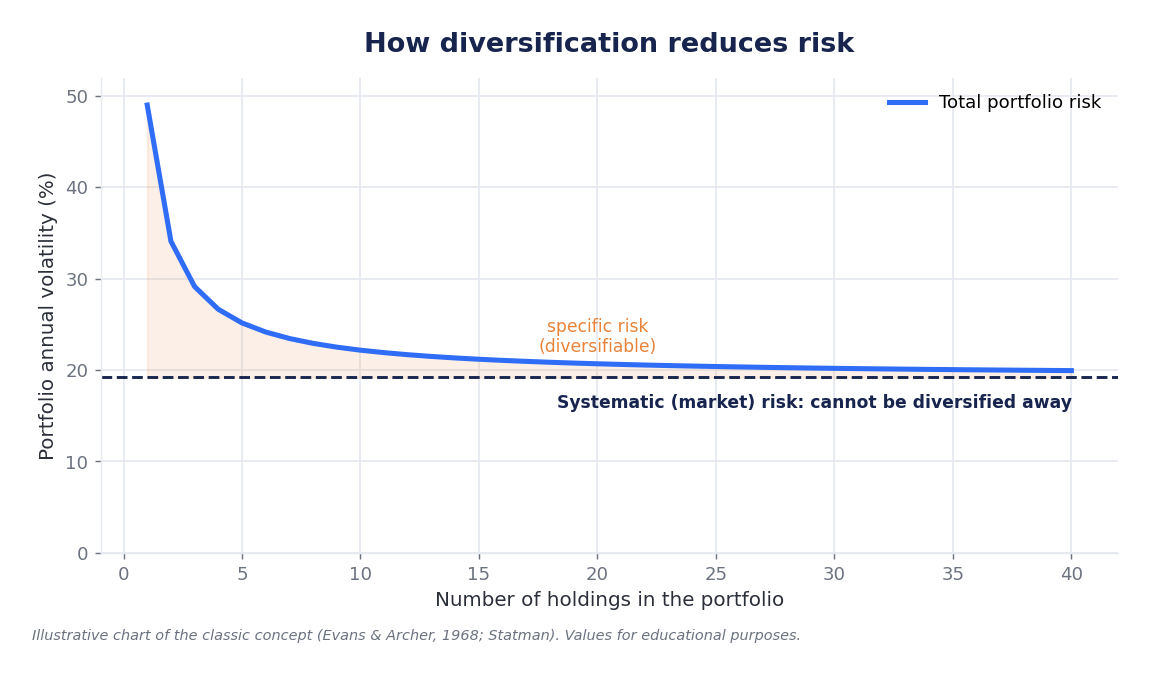

- Specific (or diversifiable) risk: tied to the individual company — a scandal, a failed product, a management mistake. This risk can be almost eliminated by spreading capital across many securities.

- Systematic (or market) risk: tied to the whole market — a recession, a geopolitical crisis, a rate hike. This cannot be diversified away: it hits everyone.

The chart shows the heart of the concept: as you add securities to a portfolio, total risk falls quickly at first, then slows and flattens onto a "floor" — market risk, which remains.

How many holdings do you really need?

One of the most surprising points is that you don't need to own hundreds of securities. Classic studies show that most of the diversification benefit is already achieved with a few dozen well-chosen holdings: beyond that threshold, adding positions reduces risk only marginally. This is where tools like ETFs come in, offering exposure to entire indices in one go.

The dimensions of diversification

Diversifying doesn't just mean "buying lots of stocks". The dimensions differ:

| Dimension | Example |

|---|---|

| By asset class | Stocks, bonds, cash, commodities, real estate |

| Geographic | European, U.S., emerging markets |

| Sector | Technology, healthcare, energy, consumer goods |

| Time | Investing regularly over time (savings plans) |

The limits: when diversification becomes a flaw

Diversification is not an absolute good. There is such a thing as "di-worse-ification": piling up so many instruments — often overlapping — that the portfolio becomes unmanageable without actually reducing risk. Owning five ETFs that track almost the same index isn't diversifying: it's duplicating. Moreover, as the chart shows, diversification does not protect against broad crashes: in deep crises many assets fall together.

The bottom line

Diversification is the most effective, low-cost defence against market unpredictability. It reduces avoidable risk, not market risk; it works even with a modest number of well-spread holdings; and it should be applied across several dimensions — assets, geography, sectors, time. It does not eliminate risk, but it makes it far more manageable.

Disclaimer: this article is for information and educational purposes only and does not constitute financial advice. Any investment decision should be assessed against your own circumstances and, if needed, with a qualified professional.