The 2026 energy transition can be told with two numbers that seem to contradict each other. On one hand, for the first time in history, the world is investing nearly twice as much in clean energy as in fossil fuels. On the other, the large listed oil majors are doing the exact opposite: slowing down on renewables and returning to oil and gas. Understanding why these two movements coexist is the key to reading the energy sector today.

The big picture: clean overtakes fossil

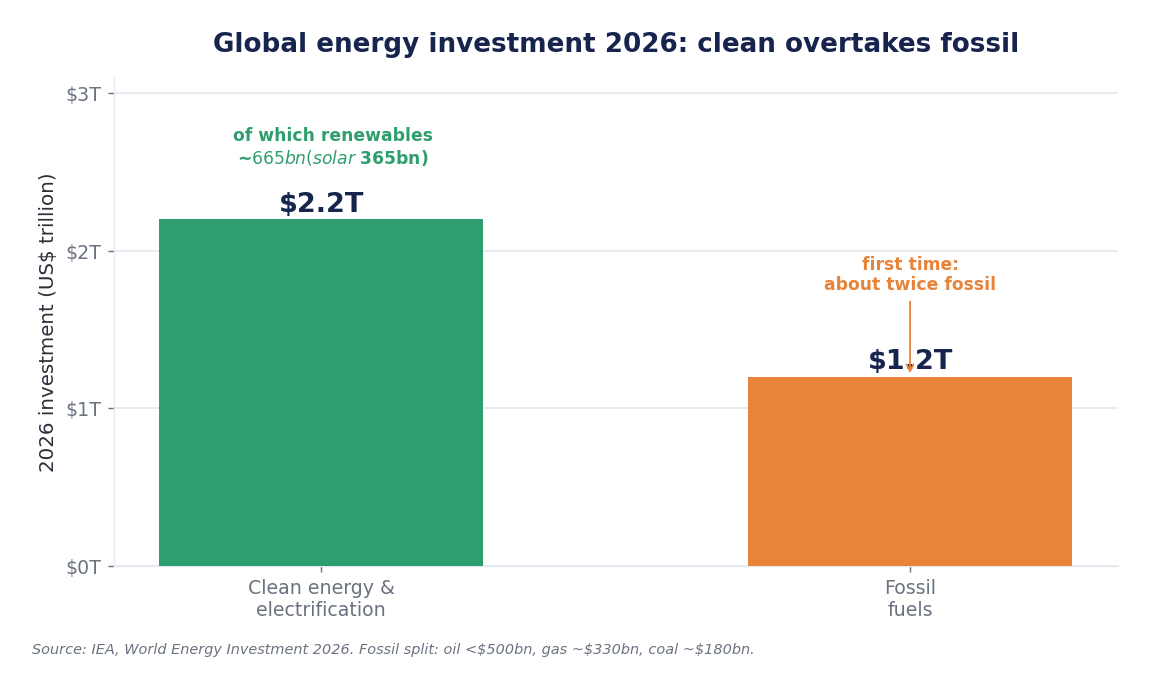

According to the International Energy Agency (IEA), global energy investment in 2026 will reach about $3.4 trillion. Of this, $2.2 trillion will go to clean energy and electrification, against $1.2 trillion for oil, gas and coal. Low-emissions technologies now account for more than 70% of investment in power generation.

The driver is solar, which alone attracts about $365 billion, within a renewables total of roughly $665 billion. On the fossil side the picture is more nuanced: oil investment stays below $500 billion for a third consecutive year, while gas (driven by US and Qatari LNG) and — surprisingly — coal are rising.

The paradox: why the oil giants are braking

If global capital rewards clean energy, why are the majors moving the opposite way? The answer is in returns. BP admitted it had gone "too far, too fast" on the transition, calling its green bet "misplaced": it will raise oil and gas spending to about $10 billion by 2027. Shell has cut renewables growth plans, seeing no competitive advantage there. ExxonMobil never strayed from hydrocarbons.

The reason is brutally simple: the median return on capital in oil is around 11%, against roughly 2% for renewables.

This is the two-speed transition: states and large institutional capital fund long-term electrification, while listed companies — under shareholder pressure for dividends and immediate returns — defend their profitable core.

The market's reading

This divergence shows up in the stock market too. In recent years traditional energy stocks have often outperformed "pure" renewables, penalised by high rates and squeezed margins. The chart below shows the performance of the US energy sector.

But beware of hasty conclusions: hydrocarbons' outperformance reflects the current cycle of rates and prices, not necessarily the long-term future. The structural direction of capital — toward electrification — remains clear.

What it means for the investor

- There is no single "energy" block: oil, gas, renewables, grids and nuclear have different drivers, risks and timeframes.

- Short versus long term: hydrocarbons offer cash and dividends today; electrification is the structural bet, but with so far more disappointing returns.

- Policy and rate risk is central: incentives, tariffs and the cost of money shift the balance more than technology itself.

The bottom line

The energy transition is neither the linear triumph of renewables nor their failure: it is a two-speed journey, in which aggregate capital races toward clean energy while listed companies defend fossil profits. For the investor, the lesson is the usual one: separate the narrative from the numbers, and the short term from the structural.

Disclaimer: this article is for information purposes only and does not constitute financial advice. Any investment decision should be assessed against your own circumstances and, if needed, with a qualified professional.